![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/04/1775434943_ai-generated-image-used-only-for-representation.jpg)

A haunting issue: 74 malls, 15.5 million square feet, and a lot of silence

Today, India is home to dozens of struggling or shuttered malls, especially in metro suburbs and smaller cities that experienced the first wave of mall construction in the 2000s.The numbers almost read like a warning sign. Out of 365 shopping malls surveyed across India, 74, roughly 20% have been classified as “ghost malls.” This together accounts for about 15.5 million square feet of vacant or underused retail space, a lot of square footage built for shoppers who no longer show up. And these are not just struggling malls with a few shuttered stores but retail spaces that have lost their commercial pulse, where high vacancy, weak footfall and a broken tenant mix have pushed them into irrelevance.What makes these malls even more haunting is what they once promised. They were built as symbols of aspiration, in a time when malls stood for modern India, cool interiors, global brands, food courts, multiplexes and weekend family outings. Back then, they were not just shopping centres; they were markers of a rising urban lifestyle. Today, many stand as quiet reminders of what happens when real estate ambition moves faster than retail reality. Where the ghosts live: West and South dominate the dead-space map

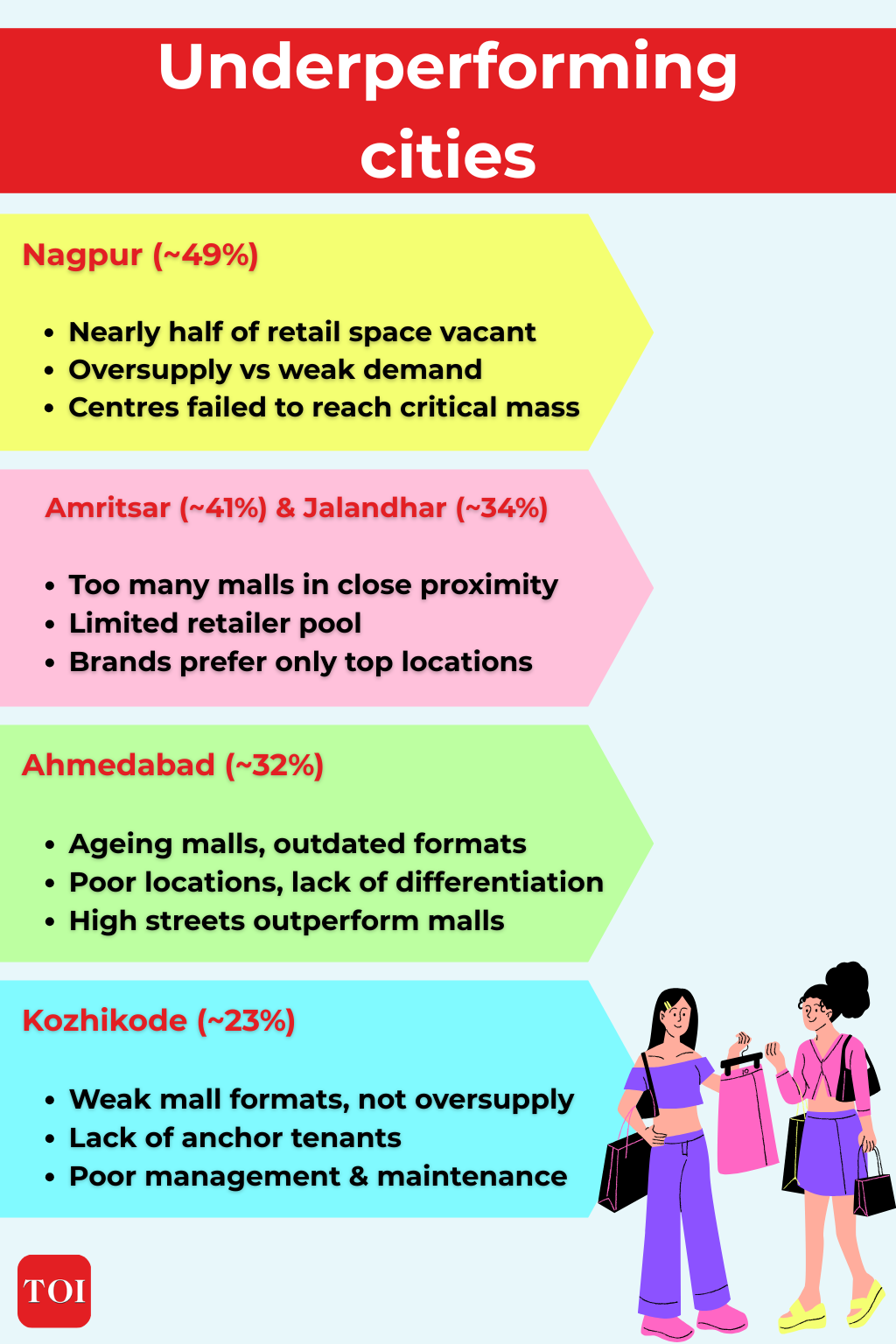

If you want to map India’s ghost malls, the dead-space geography is not evenly spread. West and South India dominate the list. These regions account for the largest concentration of non-performing or near-dead mall assets.That itself offers a strong narrative hook. Why are the “ghosts” clustering there? In many cases, these were among the earliest and most aggressive mall development markets. Cities in the West and South saw rapid mall construction during the big retail real estate push, when developers rushed to monetise urban land and consumer optimism. But scale alone did not guarantee sustainability.Why do malls die?

The rise of ghost malls in India is less about low consumer spending and more about poor planning and oversupply in certain areas. Many malls, especially in the same locality, lack differentiation, causing fragmented footfall and frequent shop closures. E-commerce accelerated the decline but isn’t the main cause. “India’s ghost malls are less a reflection of weak consumption and more a result of uneven supply expansion and gaps in asset positioning across micro-markets. Nearly 20% of malls across 30+ cities are currently under-occupied, with stress visible not just in smaller cities but also in pockets of larger urban markets,” Naveen Malpani, Partner and Consumer & Retail Industry Leader, Grant Thornton Bharat told TOI.When location misfiresOne of the biggest factors behind a mall’s success is its location and ironically, it’s often the very thing that leads to its downfall. Poor planning at the outset, such as choosing the wrong catchment or misjudging demand, has turned many shopping centres into ghost spaces. Several malls were built in areas without enough consumer base to sustain them. In smaller cities, developers in the 2000s sometimes overestimated future demand, constructing multiple shopping centres where just one would have sufficed, leaving several half-empty from the start. In other cases, too many malls emerged in the same locality, all vying for the same spotlight. When supply exceeds demand, only a few malls remain relevant, while others slowly lose footfall. Take Noida’s Great India Place, Wave Mall, and DLF Mall of India. Located close together and targeting the same shoppers, the arrival of the larger, modern DLF Mall of India shifted consumer preference, leaving older malls struggling to keep pace. During my time in Noida for graduation from 2016 to 2018, Great India Palace (GIP) was the go-to hangout spot for everyone. We’d meet there to decide on movies, food, shopping. Later, Mall of India gained popularity, but GIP remained accessible and widely visited. People would often visit both malls to compare which was better for movies, shopping, or dining. Over time, some shops at GIP began closing, and footfall gradually shifted elsewhere. The Wave Cinema at GIP still drew a few visitors, but apart from that, activity slowed. GIP was central for many years, especially in the late 2010s, but since around 2022–23, post-pandemic closures and a slowdown have gradually changed its prominence.

Harsh Shivam, a former engineering student told TOI.

Quality over quantity: retailers focus on efficiency and experience

Retailers are now prioritising efficiency and performance, revisiting leases, trimming underperforming stores, and turning outlets into experience or fulfilment centres. India isn’t lacking demand; instead, consumers are choosing quality and relevance “For retailers, this has sharpened the focus on store-level productivity and capital efficiency, with many renegotiating lease structures, rationalising store networks, and using physical stores as experience and fulfilment hubs. Ultimately, India does not have a demand deficit, it is witnessing a quality and relevance filter. The market is clearly bifurcating between high-performing, curated retail destinations and commoditised assets that are increasingly becoming obsolete,” Malpani told TOI.The great contradiction: Empty malls in a market with a retail space shortage

Here is where the story becomes both genuinely fascinating and a little absurd.India has ghost malls, but it suffers from a shortage of quality mall space.At first glance, those two facts should cancel each other out. If there is empty retail space, why do brands keep saying there is not enough space? Why are rentals in top malls strong? Why do new entrants still struggle to find the right location?The answer is simple, and powerful: not all retail space is equal. This is the contradiction that makes the ghost mall story more than a tale of collapse. India does not suffer from a pure oversupply problem. It suffers from a mismatch problem. There is dead space, yes, but often in the wrong place, with the wrong design, the wrong tenant mix, the wrong catchment, or the wrong consumer proposition. The silver lining: Dead malls can be reborn

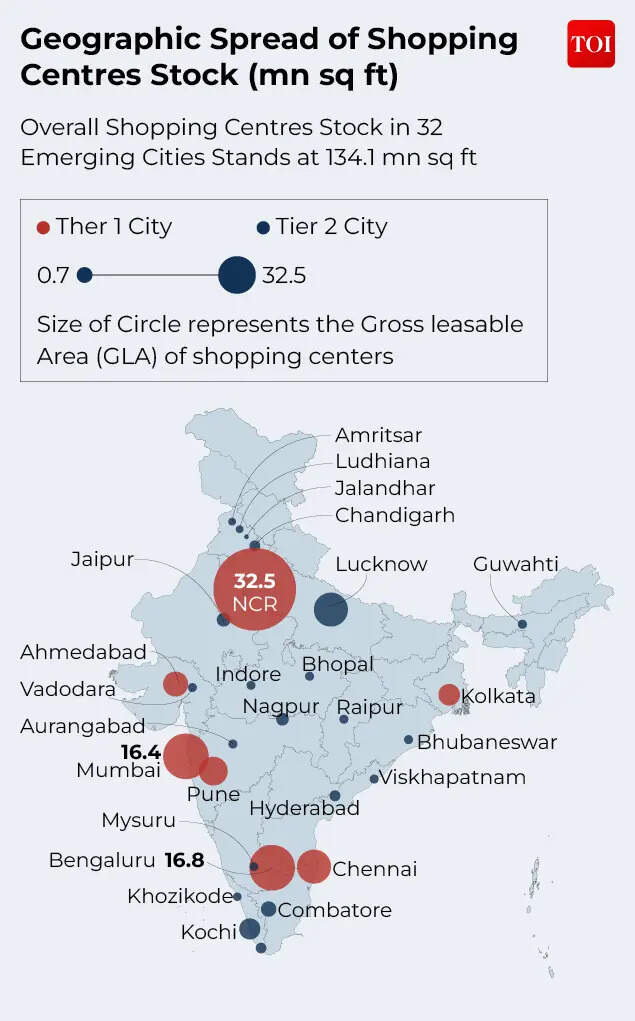

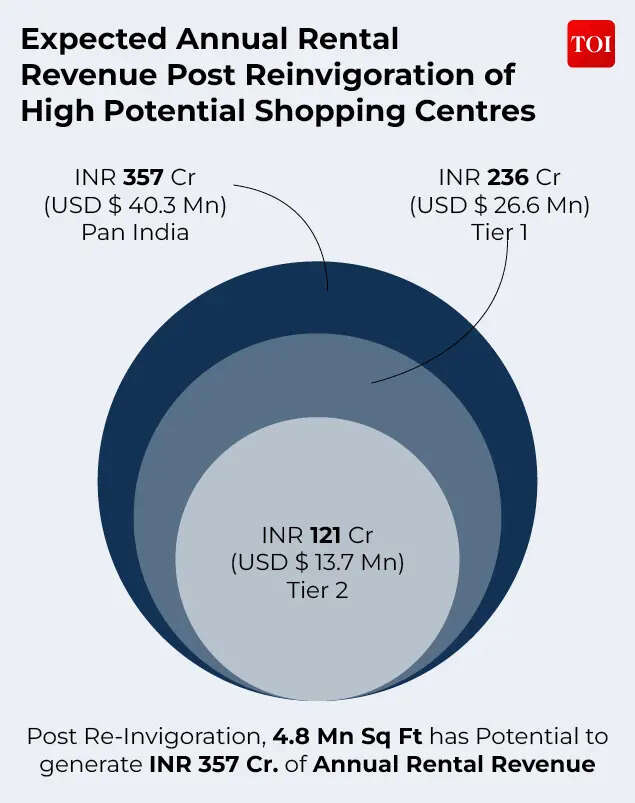

Not every ghost mall has to remain a ghost. So, what should a city do with 15.5 million square feet of empty retail space? Imagine turning old, quiet malls into bustling hotspots and making strong returns while doing it. That’s exactly the opportunity in India’s retail real estate today. Tier 1 cities hold two-thirds of the potential (INR 236 Cr), while Tier 2 cities add another INR 121 Cr. Instead of spending huge sums on building new malls, investors can revive dormant centres and unlock cash flows with projected rental yields of 5.86%.Regionally, the West and South dominate, generating 77% of projected rental revenue. But the trick is strategy: pick the right property, execute well, and these “sleeping giants” can become high-yield, value-add investments. Lessons from global markets show how revitalisation works and in India, 15 shortlisted centres across 11 cities could together produce Rs 357 Cr annually.Simply adding a few new brands, a fresh coat of paint, or a rebranded logo isn’t enough. Real revival often means rethinking the purpose of the space, resizing, re-tenanting, improving circulation, enhancing access, or even converting the mall into something entirely new. The bottom line?

The story of India’s ghost malls is not just about empty corridors and silent food courts, it’s a lesson in adaptation. While many first-generation malls failed to evolve with changing tastes, their vast spaces, central locations, and existing infrastructure hold immense potential. From entertainment hubs and co-working spaces to education centres and healthcare facilities, these “sleeping giants” can be reinvented to meet today’s urban demands. For investors and cities alike, the message is clear: with the right strategy, what once felt hollow can be transformed into vibrant, profitable destinations. The malls of yesterday may yet become the thriving landmarks of tomorrow.The takeaway? India’s retail real estate has a “second chapter” ready to be written, and the malls of yesterday could be the cash cows of tomorrow.Source link

![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/04/1775429925_stock-market.jpg)

![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/04/1775424905_1775424904_551_-.jpg)

![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/04/1775419825_modern-tvs-on-display.jpg)

![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/04/1775414749_1775414749_161_-.jpg)