![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/04/1775424905_1775424904_551_-.jpg "OPEC+ to consider output hike as US-Iran war disrupts oil supply routes")

![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/04/1775419825_modern-tvs-on-display.jpg "India Television Market: Middle East tensions to hit TV sales? Industry braces for decline as production costs rise")

![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/03/1773155658_india-energy-security.jpg)

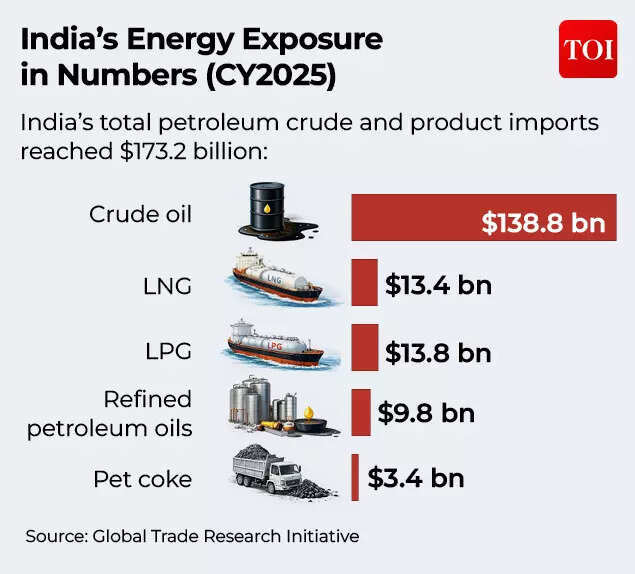

Experts note that while the domestic buffers for oil are relatively strong, LPG and LNG supplies need a boost. (AI image)

What’s the current status of India’s energy security?

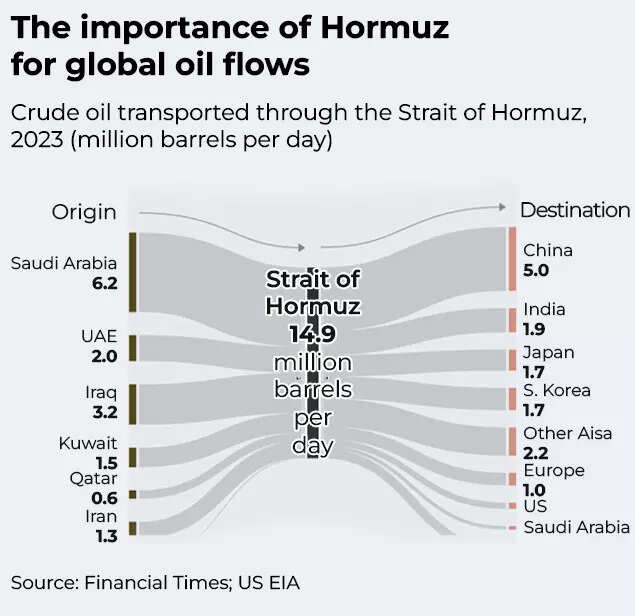

Experts note that while the domestic buffers for oil are relatively strong, LPG and LNG supplies need a boost. According to the government, India has 25 days of crude oil, its petrol and diesel can last another 25 days apart from the strategic oil reserves it maintains. Cooking gas stocks can last around 25-30 days, and liquefied natural gas stocks of around 10 days are available.India has the capacity to hold 5.33 million tonnes of crude in underground caverns at Visakhapatnam, Mangaluru and Padur – roughly 40 million barrels, or about 9–10 days of national demand. At present, around 80% of this is full. India has also stepped up purchases of Russian crude oil to tide over the immediate supply deficit.Sourav Mitra, Partner – Oil & Gas, Grant Thornton Bharat believes that India has quietly built depth into its energy security. Price volatility may be unavoidable – but the era of sudden physical shortages is steadily receding.Which new strategic reserves projects are in the pipeline?

Oil (Strategic Petroleum Phase-II): As of the latest Parliamentary review, land at Chandikhol and Padur-II was yet to be handed over by state governments, even as FY26 funding lines have been opened, so commissioning looks staggered later in the decade rather than immediate. When operational, India’s strategic petroleum reserves (SPR) capacity rises from 5.33 MMT to 11.83 MMT, taking SPR-only cover from around 9–10 days towards 20 days, depending on demand, says Sourav Mitra of Grant Thornton Bharat.LPG: The HPCL Mangalore cavern was commissioned in September 2025. This has lifted underground LPG capacity to approximately 140,000 MT (Mangalore around 80,000 MT + Visakhapatnam 60,000 MT). In practice, national ‘days of cover’ for LPG depend on above-ground tanks and import cadence, but the two caverns now provide east–west strategic anchors. LNG: The 10% terminal-level strategic buffer is at draft stage; once notified, operators would phase in additional tankage or designate buffer volumes with government call-off protocols and cost-recovery. The recent chain of force majeure notices (QatarEnergy) has sharpened the case for quick notification, as a fast, low-capex way to add a national LNG backstop.Insulating against future shocks: What should India do?

Experts stress the need for a multi-pronged strategy to deal with any future supply shocks. Apart from diversified procurement sources, domestic reserves need to be shored up to prevent both short-term and long-term supply shocks.Gaurav Moda of EY-Parthenon India says that the next phase of strategic petroleum reserves should be prioritised. “India can benefit further from acceleration of strategic expansion for Phase II that shall raise the strategic petroleum reserves to 11.83 MMT (which is an additional 17 – 18 days buffer); a separate feasibility study for six new strategic petroleum reserve locations is also underway for the next set,” he says.- Broaden supply beyond a single anchor: India has prudently extended its long-term Qatar arrangement (7.5–8.5 mtpa through Petronet) and diversified with US volumes via GAIL; even so, at the national level, concentration remains meaningful. Adding term volumes from non-Hormuz geographies (US, Australia, West Africa) so that no single source exceeds ~30–35% would be a steady next step, he says.

- Pursue equity in producing assets: China’s NOCs hold stakes in 20% in Yamal, 20% in Arctic LNG 2, 5% in Qatar NFE, 25% in Australia’s APLNG-positions that provide flexibility in tight markets. Similar minority stakes in producing assets outside Hormuz can quietly improve India’s hand over time.

- Strengthen the trading and shipping spine: GAIL’s US FOB contracts and regular swap tenders are encouraging. Scaling a trading desk (JKM/TTF/Henry Hub hedging) and building a time-chartered LNG carrier pool would help India manage arbitrage and schedules during dislocations.

- Notify the 10% LNG buffer rule and drill the protocol: Turning the draft into a notified mechanism with clear call-off, replenishment and cost-recovery rules. This will offer a quick, affordable “gas SPR” across all terminals.

- Finish SPR-II and map SPR-III: Completing Chandikhol/ Padur-II and planning a third tranche would raise government-held crude coverage closer to IEA-style 90-day norms (alongside OMC stocks) as demand grows.

- Deepen LPG resilience: With Mangalore and Visakhapatnam caverns in place, a third site and VLGC jetty upgrades can gently lift household-fuel security.

- Keep crisis playbooks ready: The current LNG squeeze saw tactical curtailments to industry and protection for priority users. Codifying a National Fuel Substitution Protocol (for temporary LPG/naphtha/FO switches) and prudent price-risk hedging at PSUs can smooth the response in future events.

Source link

![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/04/1775414749_1775414749_161_-.jpg)

![[keyword]](https://usatodaycom.com/wp-content/uploads/2026/04/1775409716_130039925.jpg)